June 16, 2022

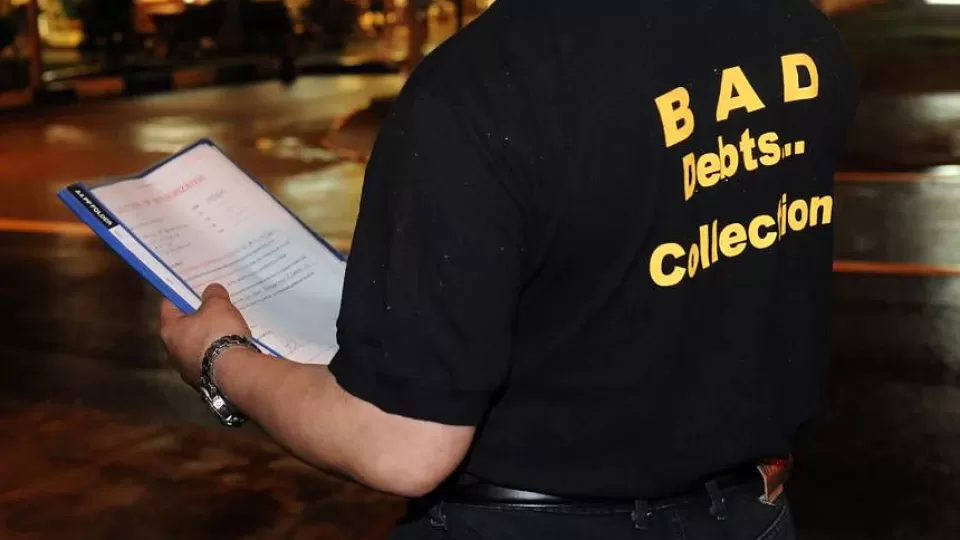

SINGAPORE – A police licence may be needed to run a debt collection agency in Singapore, one of several rules under proposed new laws to regulate their activities.

Debt collectors will also be required to first verify that the person they are collecting debt from is the debtor, under the proposed rules released by the Ministry of Home Affairs (MHA) on Wednesday (June 15).

In addition, they will not be allowed to behave in a way that is physically threatening. This includes speech, writing, signs or any visible representation, said MHA.

The ministry’s recommendations seek to address the issue of having a high number of police reports made against debt collection companies and their staff for causing alarm and nuisance to members of the public.

There were 134 such reports in 2015, which grew to 590 in 2018, before falling to 272 reports last year.

MHA said it is seeking feedback from members of the public on its proposals.

It also said it recognises that debt collection is a legitimate activity that facilitates the fulfilment of financial obligations.

“However, in view of the increasing concerns, there may be a need to institute upstream regulatory interventions on the industry, to better manage the disamenities from such activities,” it said.

First, it proposed a licensing regime where those who wish to run a debt collection business will have to first apply for a licence from the police. Those who wish to work for such companies will have to jointly apply with the company for approval.

MHA said this screening process is similar to the application process for many other regulatory regimes.

Licensed debt collection companies are required to adhere to rules such as keeping proper records of things like contracts with creditors, which will help facilitate police investigations if there are complaints.

MHA also suggested imposing a lower regulatory burden on companies whose primary commercial interest is not debt collection, but still carry out such activities to recover sums owed to them.

These companies include licensed moneylenders, banks and finance companies. They do not need police approval to operate but are required to comply with debt collection rules.

“This (class licensing framework) is based on police’s observation that the majority of reports lodged for debt collection harassment are against debt collection companies collecting debts on behalf of others, rather than companies collecting their own debts,” said MHA.

The police can impose regulatory sanctions for breaches, such as revoking the companies’ class licence, which stops them from collecting debt.

Under the proposed rules, debt collectors can only display debt notices on the debtor’s property, such as a house or car.

They are not allowed to post such notices at the debtor’s workplace or at a public place.

If a debtor has informed the collector by verifiable means that the debt is in dispute and he wishes to settle it through legal means – such as through court or mediation – the collector is not allowed to continue to try to get the money back or communicate with the debtor.

The same applies when an individual has informed the debt collection company that he is not the debtor, unless the collector is able to prove otherwise.

Members of the public who wish to give their feedback can do so via this link until June 29.