January 31, 2022

KUALA LUMPUR – OIL prices are on a tear. Just like there were in 2008 and from 2011 to 2014 going by recent memory. There is one notable difference today though. When oil prices surpassed US$100 (RM420) a barrel in those periods, there was vibrancy that was felt.

Malaysia’s coffers were growing from exports receipts of Petroliam Nasional Bhd (Petronas), which in turn contributed to the country’s fortunes and ability to fund its economic growth and expansion.

A multitude of oil and gas (O&G) service providers were created, with Petronas dishing out contracts to local companies.

Billions of ringgit in wealth creation was achieved. Fast forward to today, and the buzz that should be associated with the recent oil price climb seems to be a stifled one.

Experts are estimating that oil could go beyond US$100 (RM419) per barrel this year.

Goldman Sachs head of energy research Damien Courvalin has come out to say that that oil at US$100 (RM419) per barrel is a possibility, and it could go as high as US$110 (RM461).

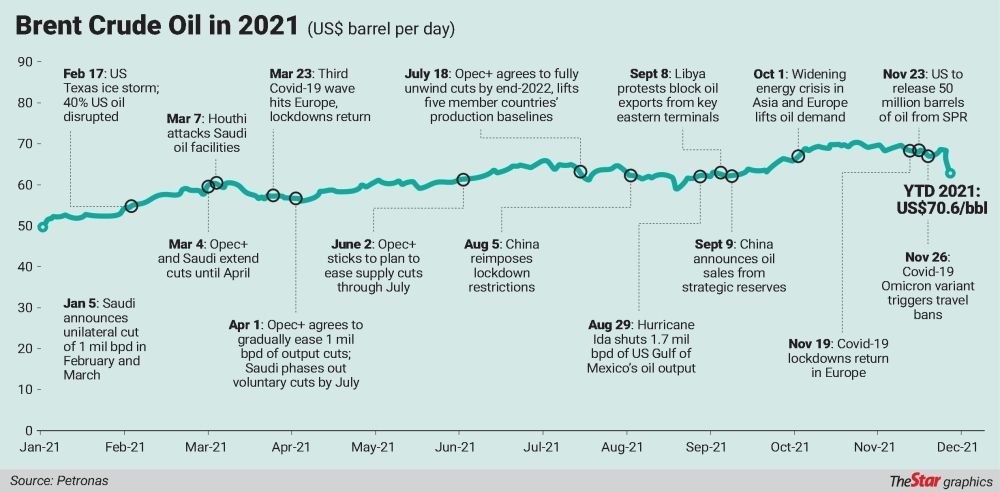

This week, the price of Brent crude oil touched US$90 (RM377) per barrel for the first time since 2014 due to the concerns about the impact of a conflict in Ukraine, and the drone strikes in the Middle East.

So how will Malaysia, as a net oil and gas exporter, benefit from the current spike in oil prices?

Socio-Economic Research Centre (SERC) executive director Lee Heng Guie says a higher oil price is generally associated with higher economic growth for Malaysia and it bodes well for the government’s coffers.

The O&G sector contributes about 6.2% of the country’s gross domestic product (GDP).

“It is estimated that for every US$1 (RM4.20) rise in oil prices, it will generate an estimated additional RM350mil in export value assuming an export volume of 13 million tonnes.

“On the government’s fiscal revenue, for every US$1 (RM4.19) rise in crude oil price, it will generate an additional RM300mil in oil-related tax revenue.

“In Budget 2022, the Treasury had estimated the price of oil at US$66 (RM276.54) per barrel.

“So based on the current spot price of US$90 (RM377) a barrel, it will generate an extra revenue of RM7.2bil,” he tells StarBizWeek.

According to the Economic Report 2021/2022, petroleum-related revenue is forecast to increase to RM43.9bil in 2022, more than half of which will be in the form of Petronas dividends.

For 2021, petroleum-related revenue stood at about RM42.5bil.

It is worth noting that Malaysia has subsidies for fuel. As such, the higher oil price would also see a higher subsidy payout by the government.

Last June, Finance Minister Tengku Zafrul Tengku Abdul Aziz said the government was expected to spend RM8bil on fuel and cooking oil subsidies in 2021, more than double the RM3.78bil originally allocated.

The government spent RM6.32bil in 2019 and RM2.16bil in 2020 in fuel subsidies.

When asked if Malaysia could experience the same growth in the past when oil prices went above US$100 (RM419) per barrel, Bank Islam Malaysia Bhd’s chief economist Dr Afzanizam Abdul Rashid says that there are multiple factors that may contribute to the prosperity of a country.

“Having abundant natural resources such as O&G reserves certainly help to increase the wealth of a country,” he says.

He explains that higher crude oil prices would give more headspace for the government to spend more, especially to boost the economy post Covid-19.

“Such expansionary fiscal policy would ensure that the economy grows more sustainably as the government can always prescribe additional spending,” he quips.

“Beyond just benefiting from natural resources, what is equally important is how the country is being managed.

“Issues surrounding governance and corruption are critically important as this determines confidence and trust among investors and the general public.

“The two years of consecutive decline in the Corruption Perception Index for Malaysia needs to be addressed holistically,” he stresses.

Impact on the ringgit

One clear winner of rising oil prices is the value of the ringgit. Lee explains that there is a positive correlation between the ringgit and oil prices although other factors play a part too, such as the United States Federal Reserve’s (Fed) monetary tightening.

He cautions that notwithstanding rising oil prices, the eventual unwinding of asset purchases by the Fed, followed by sooner than expected rate hikes will lift the US dollar’s strength against the ringgit.

“The rate-hikes expectation along with the financial volatility that it could inflict, coupled with a rise in bond yields, could reset investors’ firmer view about the US dollar and hence, lead to a softer ringgit,” he says.

On the other hand, Malaysia’s largest bank Malayan Banking Bhd (Maybank) head of forex research Saktiandi Supaat expects that the ringgit could strengthen further if the price of Brent crude oil reaches US$100 (RM419) per barrel.

“The ringgit could go higher by four to six sen from the current level. But that is assuming there is no further US dollar strength factors or weakness in global growth.

Yesterday, the ringgit fell against the US dollar at RM4.19 as the greenback gained support following a better than expected GDP growth that came in at 6.9% in the fourth quarter of 2021 against consensus estimates of 5.5%.

Underinvestment and ESG movement

While the strength of oil demand appears to be consistent since last year, which adds to the spike in prices, investment in the sector is not coming in.

A report by the International Energy Forum (IEF) and IHS Markit has claimed that the global upstream investment in the hydrocarbon sector remained depressed in 2021 at US$341bil (RM1.4 trillion), 23% below the pre-pandemic annual level of US$525bil (RM2.1 trillion).

“Oil and gas investments will need to return to pre-Covid levels and stay there through 2030 to restore market balance,” the report noted.

Many oil majors have been shifting their capital spending from traditional O&G exploration activities and going into more low-carbon emitting ventures.

Bank lending into the fossil fuel industry could be tepid in the coming years, following the global trends of increasing their “green financing” and “decarbonising their portfolios”.

Put simply, green financing is any financing activity which takes into account the impact on the environment or in other words, it refers to environmentally friendly financial initiatives.

In Malaysia, Bank Negara recently issued an exposure draft, which it says, sets out the proposed requirements and guidance on climate risk management and scenario analysis.

“The proposed specific requirements and expectations are to ensure that financial institutions strengthen the management of financial risks stemming from climate change to enhance the resilience of the financial sector against climate-related risks and to facilitate an orderly transition to a low-carbon economy,” Bank Negara says.

Maybank says it has committed to not finance any new greenfield coal activity and has enhanced due diligence requirements in place for this sector.

In no time, the banks could be making commitments to stop funding the O&G sector.

A report by Deloitte Insight states this: “A decade of unusual crude dynamics and accelerating energy transition is, in fact, prompting stakeholders and money managers of many O&G companies to wonder if there is long-term value in the fossil fuel business.”

While it expects oil demand to remain high, Deloitte Insight concurs that the high-growth phase of the oil market has come to an end.

“The compelling reality is that oil demand will likely not evaporate anytime soon.

“In fact, some accelerated energy transition scenarios still project oil demand of at least 87 million barrels per day by 2030.

“This immense gap between the extent of reliance on hydrocarbons now and a potential ‘green economy’ has created an investment, portfolio, and strategy conundrum for O&G companies – whether they should stay and capture the remaining, albeit uncertain, value in hydrocarbons or embrace the broader energy scope,” it pointed out.

Areca Capital Sdn Bhd Danny Wong suggests that players in the O&G industry take advantage of the current oil price to transform their business to be more agile and diversified into the new energy sector.

“At times, no matter the state of the industry, some businesses are able to take advantage of certain trends and shifts in operating conditions, to be more agile than others so that they are able to thrive.

“In this case, we will really like to see major energy companies being innovative and moving to the green/renewable energy space,” he says.

But perhaps the most somber analysis of the oil and gas industry is that it is an industry that has been disrupted by shale oil, which has made oil abundant and led to underinvestment in the sector by traditional oil and gas producers.

The cost of producing shale oil ranges from US$70 (RM294) and US$80 (RM336) per barrel.

This in turn means that high oil prices can hardly be sustainable over a lengthy period of time as shale producers will likely increase their production when prices are high and that in turn would bring down prices.

Meanwhile, SERC’s Lee adds that sustained high oil prices could hurt the global economy, which could then suppress demand for Malaysia’s exports.

Locally, Lee adds that there is also the fear of fuel inflation. “Fuel inflation will rise if the government decides to gradually reduce fuel subsidies. In fact, the timing of the planned fuel subsidy rationalisation is now being challenged by increasing costs and consumer inflation pressures, which have threatened businesses’ margin and households’ purchasing power during the uneven pace of recovery,” he adds.

Wong: Players in the industry should take advantage of prices.

Lee: Higher oil price bodes well for the government’s coffers.

On a monthly basis, the PPI local production rose 1.7 per cent in December. The increase was supported by the index of mining.