June 22, 2026

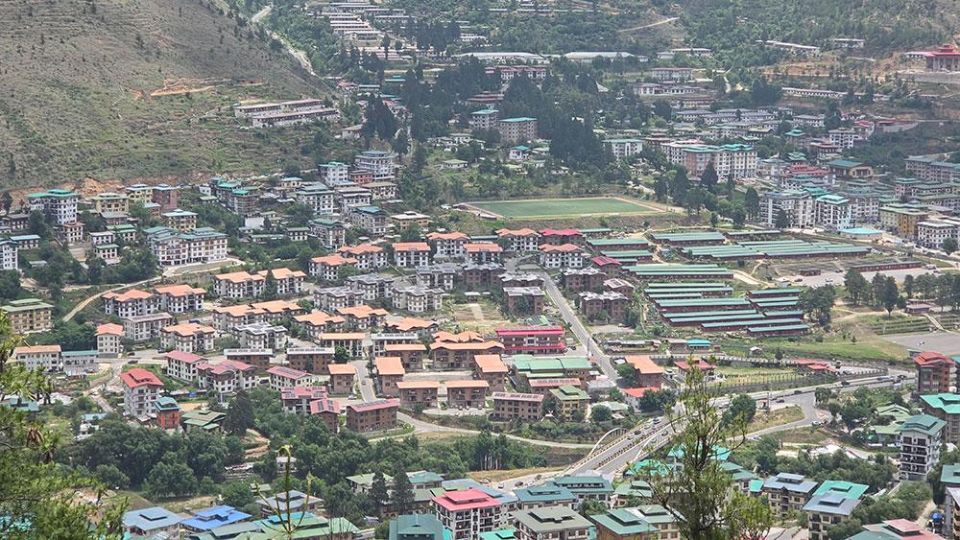

THIMPHU – Young Bhutanese have long been told that homeownership is the surest route to building family wealth, just as it was for previous generations. Today, however, that aspiration is increasingly slipping out of reach, exposing structural weaknesses in the country’s housing market that are preventing many households from accumulating long-term assets and financial security.

What was once a defining milestone of adulthood, enabling families to establish roots, build equity, and pass wealth to future generations, is becoming unattainable for a growing share of the population.

Today, many families are forced to stay in the rented apartments much longer than planned, while others continue to remain in “full-nest” households well into adulthood, with limited prospects of building equity or passing on assets.

A public-sector employee in her early 30s in Thimphu said delayed household formation is becoming increasingly common. “Everyone aspires to own a house, but it remains unattainable. What is needed is a fast-track approach to increasing the supply of affordable housing.”

Even households with stable incomes, secure employment, and sound credit histories face mounting barriers. High lending rates, rising property values, and stagnant wage growth have significantly eroded purchasing power. Housing affordability is further compounded by escalating construction costs.

Housing finance is largely inaccessible to lower- and middle-income households. Only about 9 percent of households hold housing loans, while housing microfinance products typically carry interest rates ranging from 10 to 18 percent and remain small in scale. Bhutan also lacks a nationwide homeownership programme targeted at low- and middle-income households.

Home loan interest rates currently stand at 8.13 percent for non-commercial housing and 8.93 percent for commercial housing, among the highest in the region. Banks generally finance up to 80 percent of a property’s value, requiring borrowers to provide a 20 percent down payment and repay loans over periods of up to 30 years.

Meanwhile, property prices have risen far more rapidly than incomes.

In Thimphu, modest two-bedroom apartments now sell for between Nu 5.5 million and Nu 6.5 million, while three-bedroom units typically cost between Nu 7 million and Nu 8 million. Larger apartments and duplexes command prices exceeding Nu 11 million.

One recently listed three-bedroom apartment in Changzamtog is priced at Nu 7.5 million. Purchasing such a property within a decade would require monthly savings of roughly Nu 62,500.

By comparison, the Bhutan Living Standards Survey 2022 reported a median urban household income of only Nu 28,000 per month, which would take over 22 years of total income to afford the apartment.

Construction costs further widen the gap. Based on the Bhutan Schedule of Rates 2025, a standard two-bedroom apartment house in Thimphu costs Nu 9,556.47 per sqm per metre of height. This means constructing a 2.7-metre-tall, 65 sqm house would cost about Nu 1.68 million. With the current market rate of Nu 1.85 million per decimal in Changzamtog, a small house requiring five decimals pushes the total cost to around Nu 10.93 million.

Given the market scenario, many Bhutanese living and working abroad are increasingly investing in properties overseas rather than at home.

In Australia, the dwelling price-to-income ratio is about 8.2 times, rising to 13.8 times in Sydney and 9.8 times in Melbourne, meaning a household saving its entire income could buy a home in about eight years.

More than 71,000 Bhutanese, about 10 percent of the population, currently live and work overseas, most of them young, educated, and skilled. A growing number are obtaining permanent residency, and few individuals are renouncing their Bhutanese citizenship.

Rent-driven inequality

Bhutan’s homeownership is nearly evenly split, with 53.2 percent of households owning homes and 46.8 percent renting, according to the Household Consumption and Expenditure Survey (HCES) 2025.

However, roughly 82 percent of urban households live in rented accommodation. In Thimphu, only about 17 percent of households own homes.

The Population and Housing Census of Bhutan 2017 shows a similar pattern, with 81 percent of urban residents living in rented housing, compared with 36 percent homeownership in rural areas and just 7 percent in urban areas. This reflects continued reliance on rentals in cities, with only marginal improvement in urban ownership over the past decade.

Rapid rural-to-urban migration and limited developable land have driven up urban property values, which contribute to rising cost-of-living pressures and widening inequality. Rental costs increased by 73 percent in the three years leading up to 2020, averaging 24.33 percent annually, well above the 10 percent limit under the Tenancy Act of Bhutan 2015.

A basic one-bedroom apartment in Thimphu now rents for between Nu 9,000 and Nu 10,000 per month, while three-bedroom units cost between Nu 15,000 and Nu 18,000. In Phuentsholing, rents for a standard two-bedroom apartment have climbed to more than Nu 12,000 per month, up from about Nu 8,000 earlier.

According to the Ministry of Infrastructure and Transport (MoIT), the rent cap is widely misunderstood and inconsistently applied.

Most low- and middle-income households in the bottom four income quintiles are priced out of market-rate rentals, while the private rental market lacks transparency, regulation, and affordability data.

Households in Thimphu spend around 42 percent of their income on housing, well above the 30 percent affordability threshold established under the National Housing Policy (NHP) 2020.

Economists warn that when housing costs consume such a large share of income, families are often forced to reduce spending elsewhere, rely on borrowing, or postpone investments in education and savings.

A senior economist said that homeowners or financially secure families spend less on rent and have higher disposable income, particularly for education, which is key to breaking the cycle of poverty.

“Poorer households burdened by high rent often struggle to support their children’s education, with some children taking up informal work after school, limiting study time and future opportunities,” he said.

Housing shortages are also pushing workers out of urban areas. A 2021 housing census by the Royal Institute of Governance and Strategic Studies found that 61 percent of respondents could not afford housing, while 29 percent faced shortages, forcing 5,677 Bhutanese from 2,171 households (40 percent under age 24) to live in Jaigaon, India.

Meanwhile, developers continue to prioritise commercial projects, which generally offer higher returns than residential developments, further constraining the supply of affordable housing.

The Royal Monetary Authority Report 2025 shows that credit to the housing sector accounts for 28.5 percent of total loans, amounting to Nu 73.521 billion. Commercial housing dominates with 81.6 percent, followed by residential home loans at 16.8 percent, and real estate-related loans at 1.6 percent.

Housing promise gap

Successive governments have pledged low-interest loans, affordable housing projects, and rent-to-own schemes for low-income families and civil servants. However, these commitments have lagged behind demand, with too few units delivered.

The National Housing Development Corporation (NHDCL) manages 1,129 housing units against a waitlist of over 1,500 in Thimphu. Private-sector workers, the elderly, single parents, and persons with disabilities are not eligible, while retiring civil servants must vacate tied housing without alternatives.

NHDCL’s housing stock reached 2,652 units in May 2026, up from 2,436 in December 2023.

The implementation of the NHP 2020, approved in February 2020, has also lagged behind its mandates to expand affordable housing, streamline land allocation, and introduce fiscal incentives.

Regulatory delays and limited land allocation continue to constrain supply, with new projects requiring up to 21 approvals and about 177 days to complete, according to the National Council during a recent question hour session with MoIT.

Eminent member Kesang Chuki Dorjee said implementation has fallen critically short almost six years after approval. “The deficit continues to widen across Thimphu, Phuentsholing, Samtse, and Mongar, reflecting a structural barrier that the NHP 2020 does not adequately address,” she said.

The Asian Development Bank’s Cities Development Initiative for Asia 2023 estimates Bhutan needs about 2,250 affordable housing units annually, but only 64 of a projected 1,000 baseline units had been delivered by the end of 2025.

Housing experts attribute the shortfall to a combination of high land costs, limited financing options, regulatory delays, fragmented planning systems, and rapid urbanisation. In Thimphu, land alone accounts for between 40 and 45 percent of total housing costs, substantially higher than the global norm of 20–30 percent.

Housing delivery is further constrained by weak coordination, fragmented data systems, limited local government capacity, and an underdeveloped Housing Management Information System. The sector is also dominated by small-scale builders, limiting economies of scale and affordable supply.

Additional challenges include restrictive zoning rules, scarce serviced land, speculative holding, and unbankable public land instruments, while monastic and institutional lands remain underutilised despite being in peri-urban areas.

A senior economist said government intervention through affordable housing is necessary to balance the market, as rising demand naturally drives up prices and worsens affordability pressures.

However, Nu 1.5 billion, initially allocated under the Economic Stimulus Plan for housing, was reappropriated to infrastructure priorities such as chiwog road improvement.

“The NHP 2020 is non-binding and lacks legal enforceability and dedicated budgets,” said MoIT Minister Chandra Bahadur Gurung.

Homeownership policy drive

The government is attempting to address the challenges through a series of reforms and initiatives.

The National Housing Strategy, designed to operationalise the National Housing Policy, is expected to be rolled out from July 2026 in a phased manner. The strategy will include financing mechanisms, savings-linked incentives, and measures intended to improve affordability and expand housing supply.

Lyonpo Chandra Bahadur Gurung said the ministry is working with international housing experts to develop a practical and inclusive strategy. “We are committed to ensuring that the final strategy is practical and inclusive,” he said.

Among the proposals under consideration are rent-to-own schemes, shared-ownership models, and land reforms that would extend leasehold arrangements to 99 years, with 30-year reviews. The National Land Commission introduced Strata Rules on June 2, 2026, to support leasehold use and improve housing supply.

The scheme also includes retirement provisions for civil servants, loan tracking, and savings-linked incentives to improve housing supply and affordability.

Financial measures include reduced interest rates to 5 percent and lowering equated monthly instalments to about Nu 30,000 for a Nu 7 million property in Thimphu, with banks covering around Nu 15,000 per borrower.

Under the Asian Development Bank–supported initiative, about 2,500 housing units, including 1,000 in the first phase, will be developed across 12 locations in eight dzongkhags. The first phase is financed with USD 37 million, with financing expected to close on June 30, 2028.

A USD 3 million Japan Fund for Prosperous and Resilient Asia and the Pacific Poverty Reduction grant will also support 1,000 rental housing units, alongside policy strengthening, with 184 units complete, 481 under construction, 138 planned, and 56 under the grant.

Other initiatives include the Housing Information Management System, a proposed Housing Bill 2026, national affordable housing standards, and the Gender-Responsive Monitoring and Evaluation (M&E) Framework for Safe and Livable Urban Centres in Bhutan.

The Changjiji Housing Colony supports low-income households earning below Nu 30,000 a month. Launched in 2005, the 32-unit pilot housing project promoted homeownership through long-term payment schemes, with over half of the beneficiaries owning their homes by 2026.

Meanwhile, the Tarayana Foundation has constructed 2,652 rural houses since 2003, while the government, in partnership with South Korea’s Join Together Society, has implemented a USD 5 million project in Zhemgang and Trongsa, including support for 19 vulnerable households.

Countries such as Austria, Germany, and Singapore have demonstrated that sustained government intervention, strong social housing systems, and measures to curb speculation can help maintain affordability over the long term.