June 24, 2022

ISLAMABAD – On the last weekend of May 2022, Karachi’s Movenpick hotel is buzzing with excitement. An audience of 450 individuals is ready to listen to speakers from Malaysia, the Maldives, Qatar, the UAE, the US, the UK, France, Turkey, Bahrain and Pakistan. Another 4,500 participants would join the sessions online.

This is the World Islamic Finance Forum 2022, a two-day conference organised by the Centre for Excellence in Islamic Finance (CEIF), housed at the Institute of Business Administration (IBA). One of the highlights of the events is a talk by Dr Miftah Ismail, the finance minister of Pakistan, who joins the conference via video call.

“We are working in the right direction,” Ismail says, while speaking about the Federal Shariat Court’s recent ruling stating that all banking in Pakistan should convert to Islamic banking.

“I think Pakistan as a country is moving towards full implementation of an Islamic finance system and riba-free banking,” he says. The process, he admits, may take longer than the five year timeline set by the courts.

Islamic banking in Pakistan appears to be unstoppable — while conventional banking deposits grew an average of 13 percent annually, Islamic banking deposits have grown by 42 percent in the same period. Outpacing conventional banking, and with even non-Muslim countries recognising its benefits, Islamic finance is catching up around the world. Could this be the future of banking?

Also joining virtually, Dr Murtaza Syed, acting governor of the State Bank of Pakistan (SBP), says that Islamic finance was widely recognised as one of the fastest-growing segments of global finance.

Over 70 local and international speakers take to the podium over the weekend. The eager audience participation and the scope of talks makes one thing clear: Islamic banking has arrived in a big way, and is only going to continue growing.

***

We’ve seen the transformation before our eyes.

Ask any small shop owner about how to transfer money to them and it is quite likely they will provide you with an account number in Meezan Bank, which pioneered Islamic Banking in Pakistan.

Bank branches around us have slowly changed their appearance. Language such as Sadiq (truthful), Ameen (honest), Seerat (inner beauty), Mustaqeem (straight path), Raast (sincere), Imaan (faith) and Ikhlaas (sincerity), has become more common in banks’ media messaging. Arabic calligraphy and artistic renditions of Quranic verses have appeared on walls of waiting areas. And even banks’ logos have incorporated calligraphic elements and geometric patterns associated with Islamic art.

Illustrations by Areeshah Qureshi

The staff members at these banks also dress differently of late. Most noticeably, women can be seen wearing abayas. In 2020, Faysal Bank attracted criticism on social media for issuing a new dress code mandating women to wear loose clothes and hijabs. But the criticism could not convince the bank to alter the dress code, which was clearly part of a bigger revamp.

Two years later, the ‘human resource policy’ available on the bank’s website, states that female staff should dress “elegantly with a full sleeved abaya” and must wear a headscarf covering their “entire head and hair”. “Female staff are required to follow the above attire guidelines while on duty, [and during] training and clients’ visits, as required by Islamic injunction,” the policy adds.

Other banks, including Meezan Bank, have also had similar policies in place for staff. With Meezan Bank also asking female employees to dress “elegantly” with a headscarf and abaya, “without being ostentatious”.

Those who criticised the policy had pointed out that abayas are not necessarily part of Pakistani culture. But this is all part of rebranding and conversion of conventional banks to Islamic banking (more on that later).

But while initial criticism of the Islamic banking sector suggested that it is nothing more than ‘window dressing’ on conventional banking, over the years it has truly set itself apart. And customers have followed.

Islamic banking is flourishing in Pakistan.

A GROWING NETWORK

According to a recent Fitch Ratings article, the size of the Pakistani Islamic finance industry is estimated to have crossed 42 billion US dollars (5.5 trillion rupees) by the end of the first quarter of 2022. “Islamic banks are the largest contributor to the Islamic finance industry, at 67 percent (total assets), followed by Sukuk [Islamic bonds] at 26 percent (outstanding amount), Islamic funds at 6 percent (total assets) and Takaful [Islamic insurance] at one percent (total contributions),” the article adds.

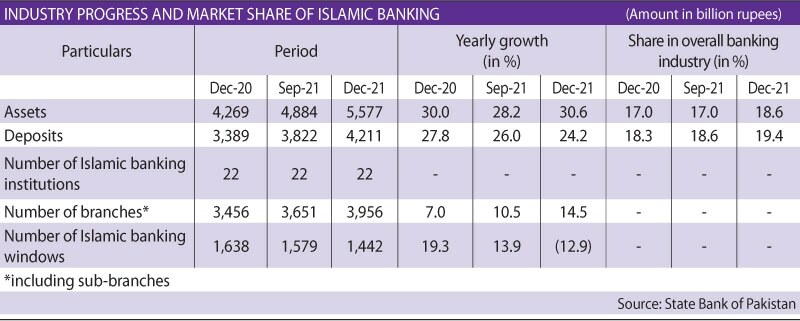

The assets and deposit values from Islamic banking are also sizeable. According to the latest SBP data, these constitute nearly 20 percent of the overall banking system.

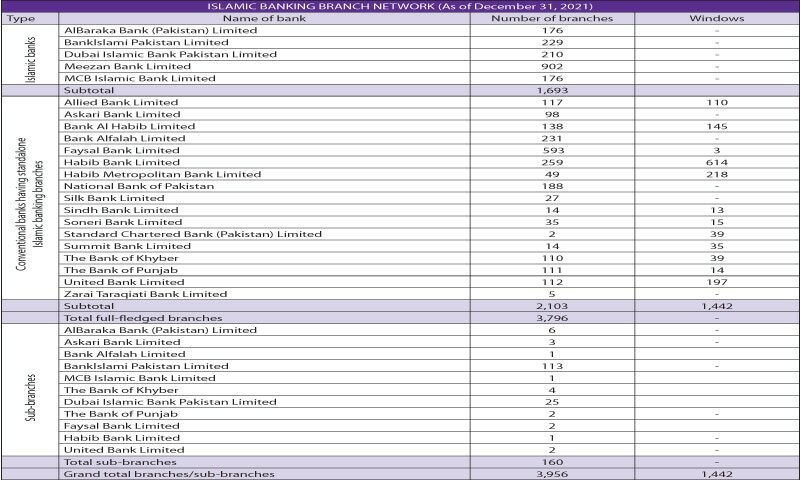

As per the SBP’s Islamic Banking Bulletin (October-December 2021), as of December 31, 2021, there were five full-fledged Islamic banks operating in the country, with 1,693 branches. Seventeen banks were also running standalone Islamic banking branches, while another 11 had Islamic banking sub-branches. The total number of branches and sub-branches stood at 3,956.

Islamic financing has been around in different forms in Pakistan for some time now. But Islamic banking, as we see it today, has made significant progress over the past two decades.

During this period, a leading Islamic bank, Meezan Bank, has succeeded in making its presence in the top five major banks of the country in terms of profitability. Muslim Commercial Bank (MCB) has established a separate subsidiary of Islamic banking, called MCB Islamic Bank Limited.

The impressive growth of Islamic banking is largely due to its increasing acceptability on religious grounds. Many in Pakistan prefer to do Sharia-compliant banking over interest-based banking.

According to the World Bank’s Global Findex database 2017, a modest 21 percent of Pakistani adults had a bank account

But the reasons for the growth are not religious alone. As global financial crises have deepened, faith in conventional banking has lowered, and this has led to a growing global interest in Islamic banking. “Somewhat perversely, the global financial crisis presented a big opportunity to the Islamic banking and finance industry,” writes Dr Mamiza Haq, a lecturer in finance at The University of Queensland in Australia, in her article Is Islamic banking more risky compared to conventional banking?

“As opposed to conventional banking, depositors to Islamic banks are entitled to be informed about what the bank does with their money and to have a say in where their money should be invested,” Dr Haq continues. “Another difference is Islamic banks avoid interest at all levels of financial transactions and promote risk-sharing between the lender and borrower.”

Due to these reasons, Islamic banking has picked up around the world. Countries including the UK, Hong Kong, Luxembourg, South Africa, China and Germany have also been exploring Islamic banking alternatives. Of course, it has also continued to pick up in Muslim countries, including Saudi Arabia, Qatar, the UAE, Kuwait and Malaysia. The progress in these countries has been much faster as compared to in Pakistan, which lags far behind when it comes to banking of any kind.

PAKISTANI USERS

According to the World Bank’s Global Findex database 2017, a modest 21 percent of Pakistani adults had a bank account. This is the lowest in the region and among countries with similar economies. This abysmally low number may have been part of the motivation to explore an alternative banking system that could attract more individuals to the banks and provide them with some financial inclusion.

A lot of research was put into understanding the needs and views of the average Pakistani. Back in 2014, SBP conducted a Knowledge, Attitudes and Practices (KAP) survey and found that 60 percent of their sample believed that the growth of Islamic banking was a demand-driven phenomenon. Very few saw the industry’s growth as a purely supply-driven phenomenon, indicating that most recognised that there is genuine demand for Islamic banking solutions.

Given the supply-demand gaps, there is a huge potential for further development of Islamic banking in Pakistan. A significant portion of demand lies among those who are still financially excluded.

Many experts believe that Islamic banking is a great way of including those who have been excluded. “Islamic finance helps promote financial sector development and broadens financial inclusion,” says the World Bank’s Islamic Finance brief. “By expanding the range and reach of financial products, Islamic finance could help improve financial access and foster the inclusion of those deprived of financial services. Islamic finance emphasises partnership-style financing, which could be useful in improving access to finance for the poor and small businesses. It could also help improve agricultural finance, contributing to improved food security.”

Of the 1.6 billion Muslims in the world, only 14 percent use banks.

The rapid growth of Islamic banking may also enhance financial inclusion by providing an alternative to those faith-sensitive Muslims who have voluntarily excluded themselves from the conventional financial system due to its interest-based nature.

“In this regard, Islamic finance can help meet the needs of those who don’t currently use conventional finance because of religious reasons,” the World Bank’s brief adds. “Of the 1.6 billion Muslims in the world, only 14 percent use banks. It can help reduce the overall gap in access to finance, since non-Muslims aren’t prohibited from using Islamic financial services.”

In Pakistan, a majority of those who use banking services also appear to be open to switching to Islamic banking. During the KAP survey, 74 percent of the banked responders said that they were willing to switch to Islamic banking, while 17 percent said they were not sure. The individuals who said they were unwilling to switch were a clear minority at nine percent.

The survey indicated that there is an overwhelming demand for Islamic banking in the country.

The conventional banking domination can mainly be attributed to their long presence and relatively wider network in both urban and rural areas, as compared to the network of Islamic banks. But this is also changing.

During the survey, the responders were also asked what factors determine satisfaction from Islamic banking services. While only just over 40 percent of responders said that they were convinced by scholars saying that Islamic banking was Sharia-compliant, more users (over 90 percent) indicated that the environment and staff at Islamic banks made them feel comfortable. Other major reasons were, expectedly, religious. Users said that Islamic products provide religious satisfaction and that these products/services were interest-free.

“Since the inception of Islamic banking in the country, conventional deposits have grown at an average of 13 percent per year,” Irfan Siddiqui, president and CEO Meezan Bank, tells Eos in an email interview. Islamic banking deposits, on the other hand, have grown at an annual average of 42 percent during the same period, he adds.

“Religious motivation has certainly remained a key influencer but it doesn’t just end there,” he says. “With a greater focus on branch experience, digital and mobile capabilities, and on offering a comprehensive range of Islamic banking products suited to the masses, we are transforming the common misperception that Islamic banking is designed only for a niche.”

Afshan Javed, a Meezan Bank customer, would agree. A resident of Karachi, Javed used to bank with HSBC (The Hongkong and Shanghai Banking Corporation Limited) Pakistan until their operations wrapped up in Pakistan and her account was automatically shifted to Meezan Bank.

At first, Javed was not sure if she preferred, or even understood Islamic banking. But over time, with the help of the bank staff, she was able to catch up. “To me, the Islamic banking model of profit-sharing, where the risk is shared by the bank and customer, makes sense,” she says. “I was also lucky that my account manager was very understanding and explained the differences between conventional and Islamic banking.”

CONVERTING TO ISLAMIC BANKING

In Pakistan, various international conventional banks have been acquired by Islamic banks including the Societe Generale Group, HSBC Bank Pakistan, HSBC Bank Oman and KASB (Khadim Ali Shah Bukhari) Bank.

Bank of Khyber, a public sector bank, has converted over 50 percent of its operations to Islamic banking. And Faysal Bank has nearly completed its transformation from the conventional system to a ‘100 percent Sharia-compliant’ one.

“The conversion of Faysal Bank from interest-based banking to Sharia-compliant [banking] is a success story not only in Pakistan but at a global level,” says Muhammad Faisal Shaikh, head of Islamic banking at Faysal Bank.

The conversion process began in 2015. “The decision was taken by the major investors of the bank for the transition from one mode of operation to another,” says Shaikh.

He adds that the transition was “monumental”. “Now the biggest conversion of a bank, at a global level, is almost complete,” he says. The bank began by converting 220 branches. Today the network has widened to 621 branches across the country. Only five branches are left and these too will be transformed in the next few weeks.

Shaikh shares that the Islamic International Rating Agency (IIRA), has deemed Faysal Bank a “first of its scale” conversion in the domain of Islamic banking.

The number of customers has been increasing with the announcement of the conversion. Reportedly, other banks also have similar plans as the Islamic finance sector goes from strength to strength.

International think tanks predict even more growth for Islamic banking and more conversions in the near future.

“Given the industry’s growth potential and strong financial performance, we expect more banks to apply for Islamic banking licences and for conventional banks to convert to fully Islamic banks,” a recent Moody’s Investors Service report says.

According to Fitch Ratings, a US-based credit ratings agency, “Islamic finance industry in Pakistan is expected to continue its growth trajectory over the medium term, driven by strong government push and steadily rising public demand for Islamic products.”

“If the court orders are implemented effectively, the Islamic finance industry could receive a large boost in the medium term,” the Fitch Ratings article adds, referring to the recent court ruling stating that all banking in the country should convert to Islamic banking.

The article goes on to acknowledge that uncertainties loom over policy implementation as court judgements on this subject were issued previously but with “limited effect” on the banking sector.

THE WAY FORWARD

While Islamic banking has been growing in Pakistan, it faces issues and challenges as well.

One challenge is that there are Islamic scholars who do not believe in any banking system and vehemently oppose Islamic banks. They even urge their followers to avoid this mode of banking and financing.

Another problem is the shortage of ‘Islamic bankers’ and other professionals who understand the system. Individuals are trained and familiarised with Islamic banking, but this too takes time. If the Federal Shariat Court ruling is implemented, there will be a dearth of professionals in this particular field.

Then there is the general lack of understanding of what constitutes as Islamic banking (see box), and what differences there are between Islamic financing and conventional banking.

Ahmed Siddiqui, director of the Centre for Excellence Islamic Finance at IBA, says that stakeholders are continuously working to raise awareness about the Islamic banking and financial system, while also addressing the misconceptions of the scholars and the general public.

Encouragingly, he mentions that specialised schools of Islamic banking have been established in Karachi, Lahore and Peshawar. These institutions have designed various courses not only for professional bankers but for scholars as well.

Universities should introduce Islamic banking as a specialised course for students of business, commerce and economics. Only then will we have future professionals trained to fill the growing demand of bankers who understand Islamic banking and are able to explain it to laypersons.

Such professionals will be essential as the industry continues to grow.

“We expect growth in Islamic banking to continue to materially outpace conventional banking [in Pakistan], reaching a market share of total assets and deposits of around 30 percent by end 2026…” predicts Constantinos Krypreos, a Moody’s Senior Vice President.

As far as Islamic banking is concerned, the future is already here.