March 2, 2022

ISLAMABAD – If you’re reading this because the headline says ‘blockchain’ and you think this write-up will provide insights on investing in cryptocurrencies, here’s a disclaimer: This piece is about blockchain technology, not just about cryptocurrencies, the latter being one of its most popular uses.

For the uninitiated, blockchain technology is essentially a digital ledger of transactions that is duplicated and distributed across a network of computer systems.

It’s not unusual for the layperson, however, to confuse anything related to blockchain with cryptocurrencies and there’s good reason too. After all, crypto was not only the first, but is also currently the largest use case of blockchain, in addition to the fact that it serves as the token and medium of exchange for virtually all applications of this technology.

Web3

But the technology has since evolved to include far more than just speculative assets and altcoins — alternative currencies launched after the success of the hugely popular Bitcoin. Web3, the internet based on blockchain, encompasses much more. To the evangelists, it represents a movement that will take control away from the government and big tech corporations and give power back to the people. Basically like Bane from The Dark Knight Rises.

Anyway, even without giving it such a dramatic flair, Web3 presents an opportunity to Pakistan to progress to newer technologies and capitalise on their demand. That can take many forms, including crypto investments, building blockchain applications and working for global Web3 startups remotely.

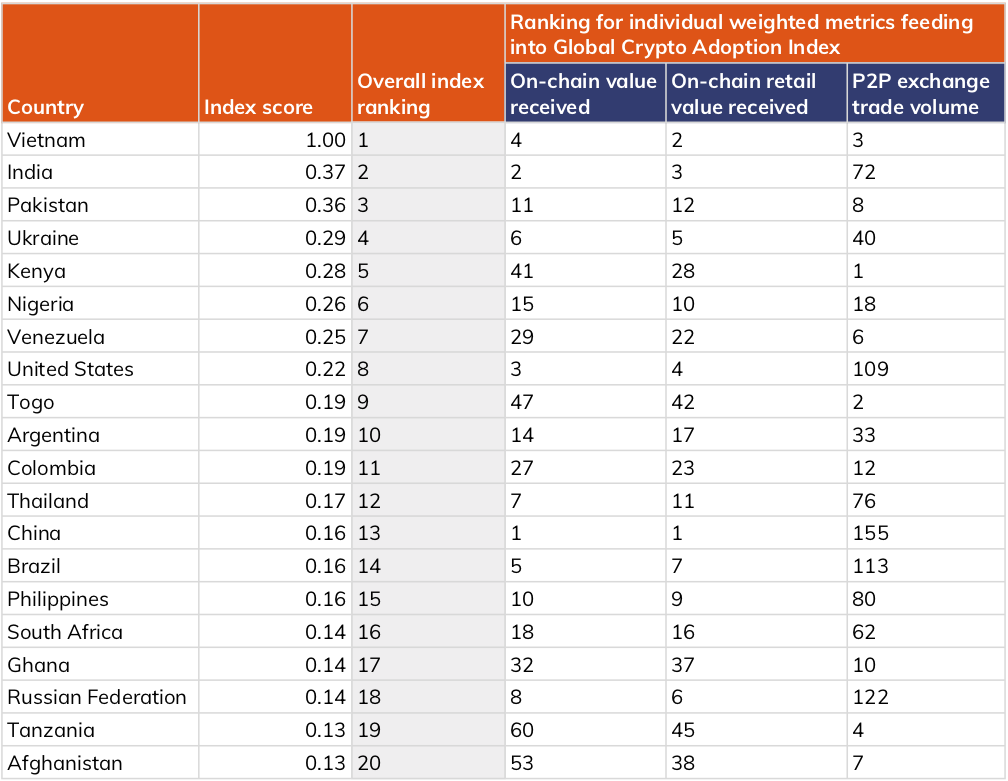

The first has taken off already as evidenced by the country ranking third on the Global Crypto Adoption Index 2021 as its traded value soared 711 per cent to around $20 billion during FY21. This was the figure that the Federation of Pakistan Chambers of Commerce and Industry misconstrued as crypto assets held by citizens and that subsequently did rounds on the local broadcast and social media.

A screenshot of the Global Crypto Adoption Index 2021. — Chainalysis.com

Irrespective of the amount of crypto assets held, we can comfortably say that Pakistanis are into this game big time. Go to any dhaba [tea stall] in pretty much any area of Karachi, for example, and you will see young men giving each other investment advice, often based on signals from Discord or Facebook groups.

This popularity, however, is scaring off regulators who have recommended a ban on crypto altogether due to its speculative nature, and more importantly dollar outflows. Another reason is obviously the money laundering and terror financing concerns which have been a big drag on the SBP ever since Pakistan was put on the Financial Action Task Force’s (FATF) grey list.

The case for regulation

Admittedly, the world of crypto is rife with frauds which makes it a sensitive issue, particularly for Pakistan due to FATF pressures. However, outright bans have never really solved any problem.

Bringing it within the regulatory ambit would not only introduce stronger Know Your Customer (KYC) requirements but also earn taxes. For example, India’s latest digital currency bill proposes to tax capital gains from crypto at 30pc, the same as betting and gambling, to account for its more speculative nature.

What the policymakers either don’t realise or willingly ignore is the emerging world of Web3.

According to CB Insights, investment raised by blockchain startups surged by 713pc to $25.2bn in 2021, of which crypto exchanges and brokerages only accounted for a quarter of the amount.

The remaining went to verticals like non-fungible tokens, decentralised finance etc. On the other hand, only two startups based out of Pakistan within this space have disclosed an investment round: dTrade’s (later renamed to Firefly Exchange) $6.4 million and Rare Sense’s $400,000 seed rounds. Amid such an interest from investors in blockchain, including in emerging markets, local upstarts are missing this gravy train.

The third aspect relates to building the talent pool for Web3 applications. True to their decentralised nature, many blockchain startups have globally distributed remote teams which opens up the possibility for engineers and other human resources in Pakistan to work for leading companies around the world and earn internationally competitive salaries.

Opportunity for Pakistan

According to a working paper by US-based think tank Atlantic Council and Paklaunch — a community group of Pakistani diaspora technologists — this alone presents a $109 billion opportunity for Pakistan over the next 20 years. It projects that even starting with a low base of 100 developers — growing at 50pc annually — earning an average of $36,000 a year, rising 10pc YoY for the first five years and 5pc thereafter, the cumulative income would be over $109bn.

Projected Web3 training and financial outcomes in Pakistan. — The Atlantic Council

“This model does not take into account additional income earned through cryptoasset appreciation over time, ownership stakes individuals may take in Web3 start-ups, and the economic multiplier effect of this additional income on the local economy,” it adds.

Of course, one can debate the individual assumptions, the overall impact, the timelines and most certainly the utopian vision of crypto bros. But what’s certain is that a sizeable activity over the internet will be on blockchain and thus blocking ourselves out of it is not going to help anyone.

The working paper by the Atlantic Council makes three recommendations. Firstly, tie in digital identity, using the National Database Regulatory Authority, to investment in crypto assets. Second, creating strong guardrails for protecting investors through awareness campaigns and clear guidelines on advertising of crypto. Finally, formalising exchanges as registered entities, tie wallets to digital identity and categorising non-registered wallets as foreign.

But before we move on to devising the regulatory framework, it’d be really helpful to know who is going to be the regulator in the first place?

In its recommendation to the Sindh High Court, the Securities and Exchange Commission of Pakistan — the regulator of capital markets — said digital assets were beyond its mandate. Neither is it the State Bank of Pakistan’s job, considering there is absolutely no scope for crypto to be treated as a medium of exchange. So who, if anyone at all, will shoulder this responsibility?